Moving on Up!

March brought continued improvement to our real estate market here in Niagara. After the last couple of years, the market is doing something strange: acting normal.

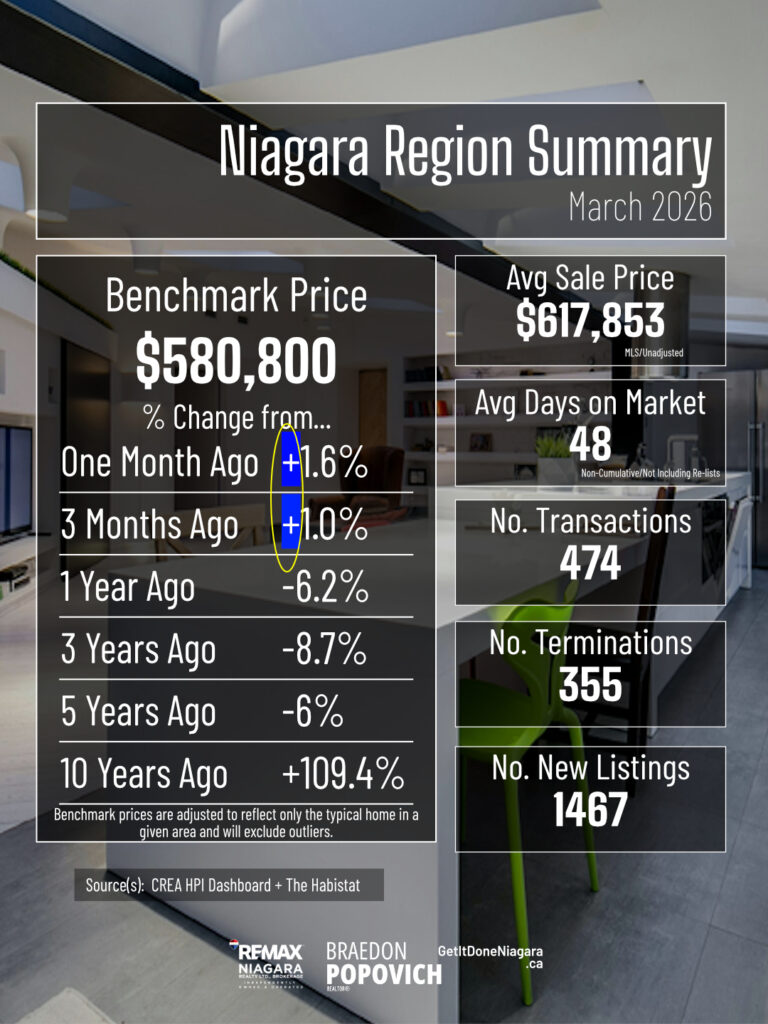

Transactions continue to outnumber terminations, meaning historical pre-pandemic norms are continuing after their return in February.

Something else has been happening though.

Benchmark Prices Increase

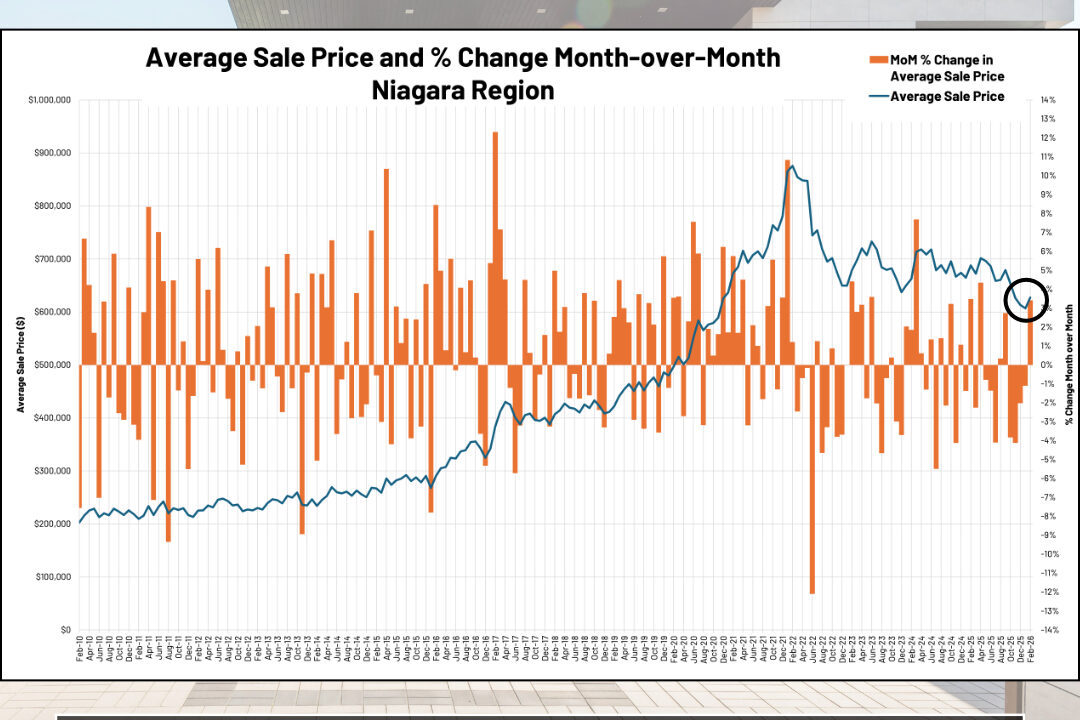

Benchmark pricing (the adjusted average to remove outliers that push averages up) has been rising slightly, as opposed to the usual drops we’ve become accustomed to. It’s another sign that our market has become healthy again, and finally returned to normalcy after catching COVID itself and crashing for a couple years!

In fact, I feel like us real estate agents have forgotten where the “+” sign was on our keyboards given all the “-” we’ve been typing this past year. Looks like this might go the other way around much sooner than I expected.

This doesn’t mean we’re headed for a hot market by any means. We’re more than likely going to see several months of small increases, then small decreases, and going back and forth for a while but balancing out at the same time.

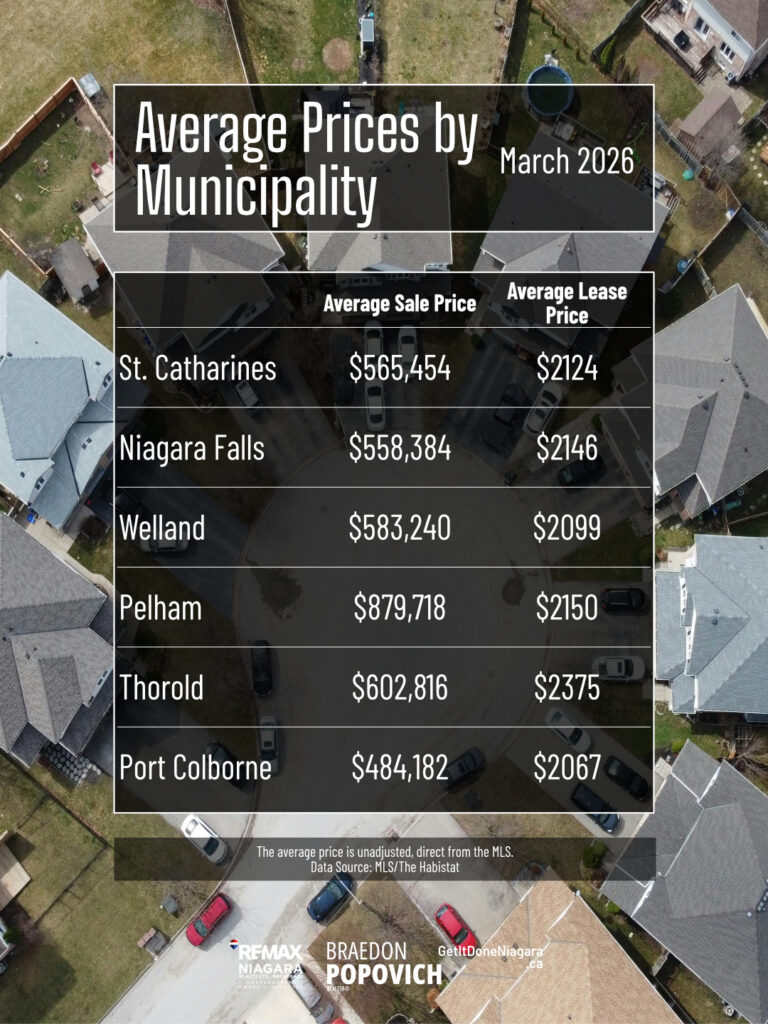

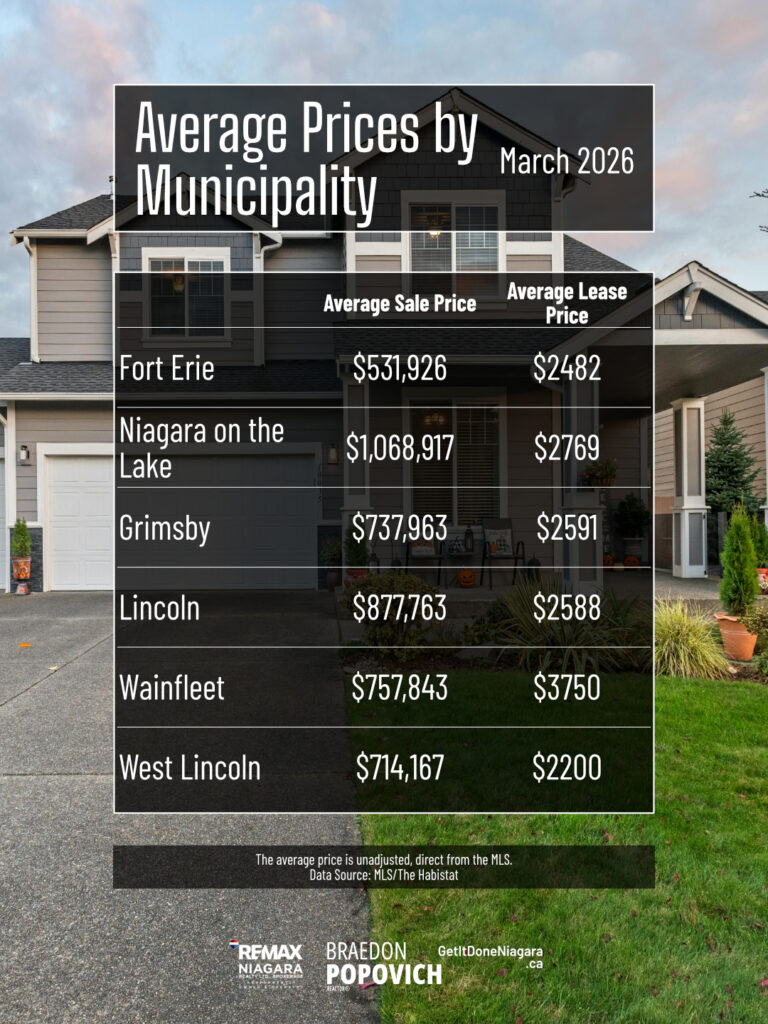

Average Prices by City

Here’s the average prices by city, now including lease prices also.

Interest Rates: Calm Now… But Not Forever

The Bank of Canada held the overnight rate steady—for now. That part wasn’t surprising for those who follow these trends like myself (I’m boring). Mid-to-long-term forecasts were pointing toward rate increases, not cuts, but this wouldn’t have happened right away anyway.

Then Trump and Iran happened. The full scale war in Iran has already pushed gas prices higher around the world. When gas prices increase, you get inflation increasing also. And inflation is often what drives interest rate decisions, especially in the post-pandemic world.

Even if the Bank of Canada doesn’t typically adjust rates for short-term/energy-related inflation, it was already expected that the overnight rate would start increasing anyway. Banks have recently started raising fixed-rate mortgages in anticipation. It’s likely coming.

The good news is that rate increases don’t push property values down to the same degree that prices rise when interest rates drop. This means that any effect on property values will be short-lived and non-severe. But this could impact the speed of our market’s recovery and is something I plan to keep a close eye on.

It’s also a good reminder that waiting for fairytale pandemic-era interest rates isn’t worth it! The house price just rises to cost you more, not less. Remember what happened in 2021! And, if those fairytale rates returned, you could always renew or refinance in the future.

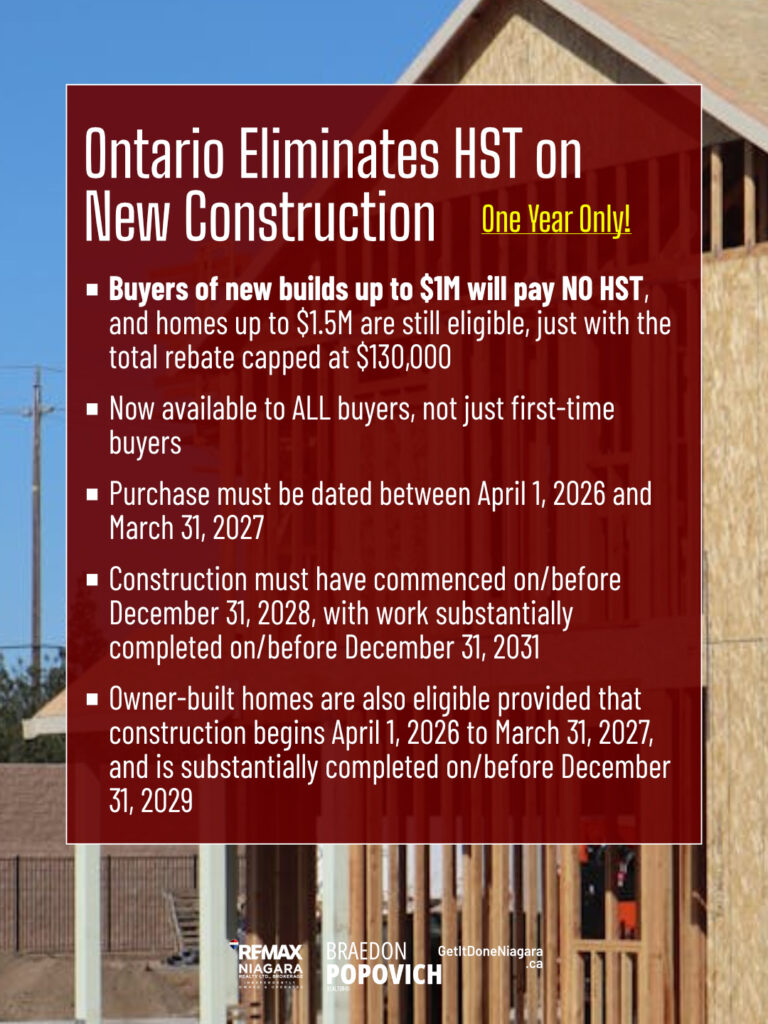

Good News for New Construction

Buyers of new builds in Ontario will end up paying NO HST for purchase prices up to $1M. The maximum rebate of $130,000 applies to builds up to $1.5M.

It’s not just first-time buyers either! All buyers will be eligible for this, even existing homeowners.

The catch? This is only for one year.

Also, the federal and provincial government have committed to spending $8.8b combined to fund municipal infrastructure. The catch? Those cities need to cut development charges, with a target of -50%. Carney and Ford also briefly talked about reducing red tape and bureaucracy, something I hope can lead into the conversation about overly restrictive and even sometimes contradictory zoning bylaws that prevent smaller lots and smaller builds, and keep younger people from having more affordable options.

Development charges have become a barrier to new construction. They even meet or exceed the $40,000 mark in some areas of Niagara when you combine both regional and municipal charges.

This is a cost that builders have no choice but to assume, and then it inevitably gets passed onto the buyers. If they are able to build at all (some smaller developers have left the industry in recent years!). Adding in financing barriers, builders hesitate before building these days. And it needs to change if we ever want to boost housing supply.

The goal is to boost both demand and supply. There will always be a demand for housing. But many buyers shy away from new builds due to higher costs and taxes.

By combining reductions in development charges with reductions in taxes, costs for buyers of new construction should drop and demand will therefore increase. Builders will also have lower upfront costs to cover, and combined with an increased demand from buyers will be more incentivized and able to build again.

We still have supply chain issues to work out, but the last few weeks have been a strong step in the right direction, and I look forward to seeing the results.